Rare Earth Elements Market Trends: Clean Energy Demand, EV Growth & Forecast to 2034

Advancements in green hydrogen infrastructure and offshore wind projects are creating new opportunities for permanent magnet usage in the Rare Earth Elements Market.

The global rare earth elements (REE) market is witnessing a transformative era, evolving from a niche industrial sector into a cornerstone of national security and environmental sustainability. These seventeen chemical elements—ranging from Neodymium used in high-strength magnets to Lanthanum in rechargeable batteries—are the "vitamins" of modern technology. As the world pivots toward a carbon-neutral economy, the reliance on these materials has shifted from being a luxury of the electronics industry to a strategic necessity for global infrastructure.

Get a Sample Report for Actionable Market Insights

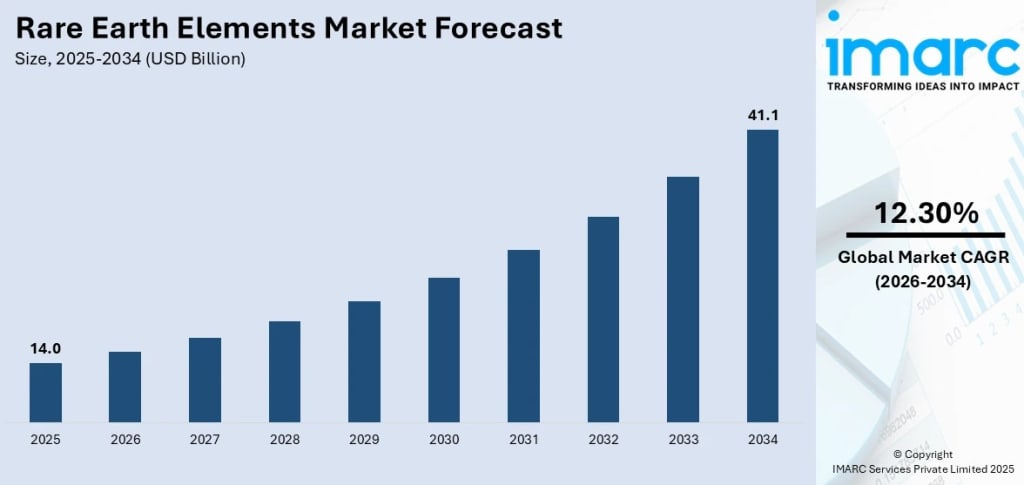

According to the latest analysis by IMARC Group, the global rare earth elements market reached a valuation of USD 14.0 Billion in 2025. This growth is underpinned by the aggressive expansion of the electric vehicle (EV) sector and the scaling of wind energy projects. Looking toward the next decade, the market is poised for significant expansion, with projections estimating a value of USD 41.1 Billion by 2034.

Market Segmentation: A Detailed Overview

The rare earth industry is highly specialized, categorized by specific elements and their diverse applications across high-tech sectors:

By Application:

Magnets: This is the largest and most critical segment, accounting for approximately 31.2% of the market share. Rare earth magnets, particularly Neodymium-Iron-Boron (NdFeB), are irreplaceable in EV motors and wind turbines due to their high energy density.

Catalysts: Widely used in automotive emission control systems (auto catalysts) and oil refining (fluid cracking catalysts).

Metallurgy and Alloys: Used to create high-strength, heat-resistant metals for aerospace engines.

Others: Includes NiMH batteries, polishing powders for glass/electronics, ceramics, and phosphors for display screens.

By Region:

China: Continues to lead the global landscape, holding over 58.3% of the market share in 2025. China’s dominance extends beyond mining into the complex refining and separation processes where it handles nearly 90% of global output.

United States: A rapidly growing hub focused on onshoring the supply chain. In 2024, the U.S. produced an estimated 45,000 tons of rare earth oxide (REO) equivalent.

Japan and Northeast Asia: Major consumers of REEs for advanced consumer electronics and precision manufacturing.

Market Growth Drivers:

The surge in demand for rare earth elements is primarily fueled by the global automotive revolution. In 2023, global electric vehicle sales surpassed 14 million units, a massive jump from just 1 million in 2017. Each EV motor typically requires between 1 and 2 kilograms of rare earth magnets to ensure high efficiency and torque. Furthermore, the aerospace sector is a significant driver; for example, GE Aviation recently invested USD 4.3 billion to enhance engine production, which relies on Praseodymium alloys for high-strength components. This shift toward high-performance, lightweight machinery makes REEs indispensable for modern mobility and industrial efficiency.

Another pivotal driver is the unprecedented focus on national defense and strategic stockpiling. Modern military hardware is heavily dependent on these materials; a single F-35 fighter jet requires roughly 417 kilograms of rare earth materials for its flight control systems and radar. Consequently, the U.S. Department of Defense has aggressively funded domestic projects, such as the USD 288 million award to Lynas USA to build a rare earth oxide separation facility. This intersection of military readiness and supply chain security ensures a steady, high-value demand for heavy rare earths like Dysprosium and Terbium, which are vital for high-temperature defense applications.

Market Trends:

A defining trend in the current market is the massive influx of government incentives aimed at breaking the "refining bottleneck." In 2025, the U.S. government revealed nearly USD 1 billion in funding specifically targeted at domestic critical mineral initiatives. A standout example is the "10X" project by MP Materials in North Texas—a USD 1.25 billion investment supported by local and federal grants. This facility aims to produce 10,000 metric tons of NdFeB magnets annually by 2028. This trend of "onshoring" is mirrored in Brazil, where the government is evaluating 56 business plans for critical minerals with a fund of BRL 45.8 billion to decentralize the global supply chain.

Moreover, the industry is witnessing a shift toward "Green Extraction" and circular economy practices. Mining companies are moving away from chemical-heavy traditional methods toward sustainable alternatives like bioleaching and recycled water systems. For instance, the Penco Module project in Chile is utilizing a process that operates with 100% recycled water, targeting a production of up to 1,700 tonnes of minerals per year. Additionally, major tech players like Apple have signed long-term agreements to source magnets made from recycled materials. This focus on ESG (Environmental, Social, and Governance) standards is becoming a prerequisite for securing long-term contracts with global OEMs.

Recent News and Developments in Rare Earth Elements Market

MP Materials & Department of Defense Partnership (July 2025): The Pentagon became a key stakeholder in MP Materials through a multibillion-dollar package to accelerate the buildout of a fully integrated U.S. magnet supply chain.

China’s Export Controls (October 2025): Beijing introduced new regulations requiring downstream producers to certify the source of every rare earth atom in finished goods. This move caused a temporary spike in Dysprosium prices for European wind turbine manufacturers.

Nidec & Noveon Magnetics Agreement (February 2025): A five-year deal was signed for the supply of 1,000 tons of rare earth magnets for industrial automation, highlighting the growing demand for precision robotics.

Brazilian Export Milestone (Early 2025): Brazilian rare earth exports to China tripled compared to the previous year, following the discovery of the "district-scale" Pelé project in Bahia state.

Texas Round Top Success (January 2025): USA Rare Earth successfully produced a sample of 99.1% pure Dysprosium dioxide, a critical milestone for domestic heavy rare earth production.

The Rare Earth Elements market is no longer just a mining story; it is a high-stakes race for technological sovereignty and climate goals. As industries move toward 2030, the ability to secure these materials through innovative recycling and diversified mining will define the winners of the green energy era.

About the Creator

Rahul Pal

Market research professional with expertise in analyzing trends, consumer behavior, and market dynamics. Skilled in delivering actionable insights to support strategic decision-making and drive business growth across diverse industries.

White-Label vs. Custom Crypto Exchanges Under MiCA - And How Smart Founders Prepare?

The European crypto market is entering a new phase of maturity. With the implementation of the Markets in Crypto-Assets (MiCA) regulation, the EU is rapidly becoming one of the most structured and institutionally trusted digital asset ecosystems in the world. Analysts estimate that compliant exchanges operating under MiCA could collectively process over €1 trillion in annual trading volume by 2028, driven by institutional participation and regulatory clarity.

By Nia Higgins5 days ago in 01

Cassie and Johnny

I’m the kind of dame you notice. I’m no femme fatale, but you can’t ignore me, at least not until I warn you about what’s coming, then everybody ignores me. Hell, they usually blame me afterwards and give Johnny all the credit for saving the day, but my Johnny couldn’t save a seat at the movies without my help. Sure, he’s brawny, but brainy? Not so much. Like that time I asked him to spot me five bucks, and he said he didn’t see it anywhere on me, and believe you me, he looked but good.

By Harper Lewis5 days ago in Critique

Comments

There are no comments for this story

Be the first to respond and start the conversation.